Рынок электрических зубных щеток 2026: размер, тенденции и возможности OEM

A data-driven market analysis for brand owners, retailers, and investors exploring the global electric toothbrush industry — with strategic OEM entry points.

Executive Summary of the Electric Toothbrush Market

The global electric toothbrush market has entered a phase of accelerated growth, expanding from $3.2 billion in 2020 to $4.36 billion in 2024. By 2030, the market is projected to reach $6.82 billion, representing a compound annual growth rate (CAGR) of 7.8%. This expansion is driven by several converging forces: rising consumer awareness of oral health's connection to systemic wellness, rapid technology integration including AI and Bluetooth connectivity, and the growing willingness of emerging-market consumers to invest in premium personal care devices.

For brand owners, retailers, and investors, the electric toothbrush market presents a compelling entry opportunity. The gap between premium branded products ($150–$350 retail) and the actual manufacturing cost ($8–$25 per unit) creates significant margin potential for private label and OEM strategies. Moreover, the shift toward direct-to-consumer (DTC) distribution has lowered the barriers to market entry, enabling new brands to reach global audiences without traditional retail channel constraints.

From an OEM manufacturing standpoint, China — and specifically the Shenzhen-Dongguan corridor — remains the dominant global production hub, accounting for an estimated 70% of worldwide electric toothbrush output. Manufacturers in this region offer vertically integrated supply chains, rapid prototyping capabilities, and increasingly sophisticated R&D capacity — all of which position the electric toothbrush market for continued expansion well beyond basic contract manufacturing.

Key Findings at a Glance

- Global market valued at $4.36B (2024), growing to $6.82B by 2030 at 7.8% CAGR

- Sonic toothbrushes now hold ~55% market share vs. 45% for rotating-oscillating

- North America and Europe account for 65% of global revenue combined

- Asia-Pacific is the fastest-growing region, with China's domestic market up 12.4% YoY

- Smart/app-connected toothbrushes represent 28% of total market and growing at 14.2% CAGR

- OEM unit costs range from $4–$35 depending on technology level and volume

- Sustainability features command 15–25% price premium in European markets

- DTC subscription models drive 3.2x higher customer lifetime value vs. one-time purchase

Global Market Size & CAGR 2024–2030

Historical Growth Trajectory (2020–2024)

The electric toothbrush market demonstrated remarkable resilience through the COVID-19 pandemic. While initial supply chain disruptions in early 2020 temporarily constrained production, the heightened consumer focus on personal hygiene actually accelerated adoption. Market value grew from $3.2 billion in 2020 to $3.68 billion in 2021 (+15.0%), $3.96 billion in 2022 (+7.6%), $4.18 billion in 2023 (+5.6%), and $4.36 billion in 2024 (+4.3%). The deceleration in growth rate through 2023–2024 reflects market maturation in developed regions, partially offset by accelerating growth in emerging markets.

Projected Growth: 2024–2030

Looking forward, the market is forecast to maintain steady expansion. Industry analysts at Grand View Research project the market will reach $4.70 billion in 2025, $5.10 billion in 2026, $5.52 billion in 2027, $5.95 billion in 2028, $6.38 billion in 2029, and $6.82 billion in 2030. This trajectory implies a consistent CAGR of approximately 7.8%, driven by technology upgrades, geographic expansion, and the replacement cycle for connected devices.

Sub-Segment Breakdown: Sonic vs. Rotating-Oscillating

The two dominant motor technologies — sonic vibration and rotating-oscillating — continue to compete for market share. Sonic toothbrushes, led by Philips Sonicare and a growing number of OEM brands, currently hold approximately 55% of the global market by revenue. Their advantage lies in broader brush head coverage, quieter operation, and the perceived premium positioning. Rotating-oscillating toothbrushes, pioneered and still dominated by Oral-B (Procter & Gamble), hold approximately 45%. Both technologies have demonstrated comparable clinical efficacy in plaque removal, though consumer preference increasingly favors sonic technology for its lighter feel and sleeker design profiles.

The price differential is notable: the average selling price (ASP) for sonic toothbrushes is approximately $85–$110 at retail, compared to $60–$85 for rotating-oscillating models. This premium translates directly to higher margins for OEM partners producing sonic devices, though the manufacturing complexity is marginally greater.

Regional Market Size Data

The following table presents the estimated regional breakdown of the electric toothbrush market across three key years, illustrating both the current distribution and projected growth trajectories.

| Регион | 2024 Market Size | 2026 Estimate | 2030 Projected | CAGR |

|---|---|---|---|---|

| North America | $1.53B | $1.78B | $2.31B | 7.2% |

| Europe | $1.31B | $1.53B | $2.05B | 7.8% |

| Asia-Pacific | $1.09B | $1.35B | $1.91B | 9.8% |

| Latin America | $0.22B | $0.26B | $0.34B | 7.5% |

| Middle East & Africa | $0.21B | $0.25B | $0.34B | 8.5% |

| Global Total | $4.36B | $5.17B | $6.95B | 8.1% |

Sourcing Electric Toothbrushes for Your Brand?

Relish Technology provides end-to-end OEM manufacturing — from industrial design and prototyping through production, certification, and global logistics. Request a customized quote with your specifications.

Get Your Manufacturing QuoteMarket Drivers: What's Fueling Growth

Rising Oral Health Awareness

The connection between oral health and systemic conditions — including cardiovascular disease, diabetes, and Alzheimer's disease — has moved from academic literature into mainstream consumer awareness. The World Health Organization's 2022 Global Oral Health Report highlighted that 3.5 billion people worldwide suffer from oral diseases (WHO, 2022), creating a powerful public health narrative that benefits the entire oral care industry and the electric toothbrush market in particular. Dental professional recommendations have become a primary purchase driver, with 64% of electric toothbrush buyers in North America citing their dentist's recommendation as a key factor (ADA Consumer Survey, 2024).

Social media has further amplified awareness. Dental health content on platforms like TikTok and Instagram generates billions of views annually, with electric toothbrush reviews, comparisons, and "before and after" results becoming a major content category. This organic marketing channel has significantly lowered customer acquisition costs for new DTC brands.

Smart/IoT Integration

The integration of Bluetooth connectivity, mobile applications, and AI-powered analytics has transformed the electric toothbrush from a simple hygiene tool into a connected health device. Smart toothbrushes now represent approximately 28% of total electric toothbrush market revenue, and this share is growing at 14.2% annually — nearly double the overall market growth rate. Features such as real-time brushing feedback, zone-by-zone coverage mapping, and personalized coaching recommendations create a compelling value proposition that justifies premium pricing.

The IoT trend also creates a data ecosystem. Brands with connected toothbrushes gain access to anonymized brushing behavior data that informs product development, replacement head subscription timing, and targeted marketing. This data advantage creates a significant competitive moat that legacy brands are actively building.

Aesthetic Dentistry Trends

The global aesthetic dentistry market, valued at $26.6 billion in 2024, is creating a powerful halo effect for the electric toothbrush market. Consumers investing in clear aligners, veneers, and whitening treatments are highly motivated to maintain their results, and dental professionals consistently recommend electric toothbrushes as part of post-treatment care routines. The Invisalign patient base alone represents approximately 12 million cumulative users globally — a built-in market for premium oral care devices.

Aging Population Demographics

Global population aging is a structural tailwind for electric toothbrush market growth. By 2030, an estimated 1.4 billion people worldwide will be aged 60 or older (UN DESA, 2023). Electric toothbrushes are particularly beneficial for elderly users due to ergonomic advantages, built-in timers that compensate for cognitive decline, and pressure sensors that protect receding gums. Japan, where electric toothbrush penetration already exceeds 50%, demonstrates the market potential of an aging demographic.

Key Electric Toothbrush Market Trends in 2026

Subscription Models

The replacement head subscription model has become one of the most significant business model innovations in the electric toothbrush market and the broader oral care industry. Dentists recommend replacing brush heads every three months, creating a natural recurring revenue opportunity. Leading brands report subscription attachment rates of 25–40% for smart toothbrush purchases, with average customer lifetime values 3.2x higher than one-time purchasers. The subscription model also addresses one of the biggest OEM challenges — customer retention — by creating ongoing touchpoints that reinforce brand loyalty.

App-Connected Toothbrushes

Mobile app connectivity has moved from a premium feature to an expected feature in the electric toothbrush market's mid-range segment ($50–$120 retail). In 2026, over 65% of new electric toothbrush models launched in North America and Europe include Bluetooth connectivity. The quality of companion apps has become a key differentiator, with brands competing on AI coaching accuracy, gamification elements, integration with health platforms (Apple Health, Google Fit), and family account management.

For OEM manufacturers, the app development component represents both a challenge and an opportunity. Developing a polished, reliable iOS/Android application requires specialized software engineering capabilities that many hardware-focused factories lack. This gap creates opportunities for manufacturers like Relish Tech that can offer integrated hardware-plus-software solutions.

Sustainability: Bamboo, Recyclable Materials, and Beyond

Environmental consciousness is reshaping product design across consumer electronics, and oral care is no exception. In 2026, sustainability-focused features in the electric toothbrush market command a 15–25% price premium in European markets and are increasingly expected in North America. Key sustainability innovations include:

- Replaceable battery designs that extend product lifespan from 3 years to 5+ years

- Recyclable brush heads using plant-based bristles and bio-plastic housings

- Reduced packaging — elimination of single-use plastics in favor of recycled cardboard

- Carbon-neutral manufacturing commitments, increasingly required by European retail buyers

- Take-back and recycling programs for end-of-life devices

Premiumization vs. Affordability

One of the most interesting dynamics in the electric toothbrush market in 2026 is the simultaneous growth at both ends of the price spectrum. The luxury segment ($200+) continues to expand with ultra-premium features like AI-powered diagnostics, ceramic brush heads, and designer collaborations. Simultaneously, the value segment ($15–$30) is experiencing explosive growth in emerging markets and through discount retailers. The middle segment ($60–$120) is under pressure from both directions, pushing brands to either innovate into premium territory or optimize for volume at accessible price points.

Electric Toothbrush Market: Competitive Landscape

Top Global Brands

The electric toothbrush market features a mix of established multinational corporations and emerging DTC challengers. The competitive hierarchy in 2026 looks as follows:

- Philips Sonicare (Koninklijke Philips N.V.): Estimated 28–30% global market share by revenue. Dominant in North America and Western Europe, with a strong position in the premium and mid-premium segments. Their Sonicare app ecosystem is the most mature in the industry.

- Oral-B / Braun (Procter & Gamble): Estimated 25–27% global share. Leading position in rotating-oscillating technology. Strong pharmacy and retail channel presence. The iO series represents their premium push, while the Pro/Smart series anchors the mid-range.

- Panasonic (Panasonic Corporation): Estimated 8–10% share, with particular strength in Japan and other Asian markets. Known for compact travel-friendly designs and high build quality.

- FOREO: Estimated 5–7% share, commanding the ultra-premium segment ($200–$400). The ISSA series differentiates with medical-grade silicone brush heads and bold design language.

- Colgate-Palmolive (Colgate Hum): Estimated 4–5% share, leveraging massive FMCG distribution channels. The Hum brand targets the entry-to-mid smart toothbrush segment at accessible price points.

- Emerging DTC Brands: Collectively 8–12% share and growing rapidly. Notable players include Burst Oral Care, quip, Snow, and various regional brands. These companies compete primarily on brand storytelling, subscription models, and social media marketing.

Private Label and OEM Opportunity

Despite strong brand presence, the electric toothbrush market remains accessible to new entrants. Retailer private label programs (e.g., Target Up&Up, CVS Health, Boots) account for an estimated 6–8% of global sales and are growing. The gross margin on private label electric toothbrushes — typically 55–70% at retail — makes them highly attractive for retailers seeking to differentiate their oral care sections.

For OEM partners, the opportunity is not limited to private label. Dental professional lines, corporate wellness programs, hotel amenity partnerships, and specialty niche brands (e.g., orthodontic-specific, kids-focused, travel-focused) all represent viable market entry points that avoid direct competition with the Philips and Oral-B duopoly.

Regional Deep Dive

North America

North America remains the world's largest electric toothbrush market at $1.53 billion in 2024. The United States alone accounts for approximately $1.35 billion, with household penetration of electric toothbrushes reaching an estimated 42–45% in 2025. The Canadian market contributes approximately $130 million, with slightly higher per-capita penetration due to universal dental insurance coverage and stronger dental professional referral patterns.

Key characteristics of the North American market include dominant e-commerce channels (Amazon accounts for an estimated 35–40% of online electric toothbrush sales), strong subscription model adoption, and premiumization trends. The average retail price for electric toothbrushes in the US has increased from $62 in 2020 to $78 in 2025, reflecting the shift toward smart-connected models.

Europe

Europe's electric toothbrush market reached $1.31 billion in 2024, with significant variation across national markets. Германия is the largest European market at approximately $320 million, with household penetration around 38% and strong pharmacy-channel presence. The United Kingdom follows at approximately $260 million, with the highest e-commerce penetration in Europe and rapid DTC brand growth. France represents approximately $190 million, with growth accelerating as pharmacy recommendation rates improve.

The European electric toothbrush market's dynamics are heavily influenced by sustainability requirements. The EU's EcoDesign Directive and packaging reduction mandates are reshaping product specifications for all manufacturers selling into the region. Brands that can demonstrate environmental credentials — recyclable materials, reduced packaging, repairability — have a measurable competitive advantage.

Asia-Pacific

The Asia-Pacific region is the engine of global electric toothbrush market growth, with a $1.09 billion market in 2024 projected to nearly double to $1.91 billion by 2030. China is the standout — the domestic market reached approximately $460 million in 2024 and is growing at 12.4% annually. China's e-commerce ecosystem (Tmall, JD.com, Pinduoduo) enables rapid brand building and product testing at scale. Япония remains the world's most mature Asian market with household penetration exceeding 50%, valued at approximately $280 million. Южная Корея ($120 million) and India ($95 million, growing at 18% CAGR) round out the major markets.

Emerging Markets

Brazil, Mexico, and Southeast Asia represent the next wave of growth. Brazil has a population of 215 million with electric toothbrush penetration below 10%, creating enormous headroom. Southeast Asia — particularly Thailand, Vietnam, and Indonesia — is benefiting from rising middle-class consumption and aggressive e-commerce expansion by Chinese OEM brands. These markets favor affordable models in the $15–$35 range, making them ideal targets for cost-optimized OEM production.

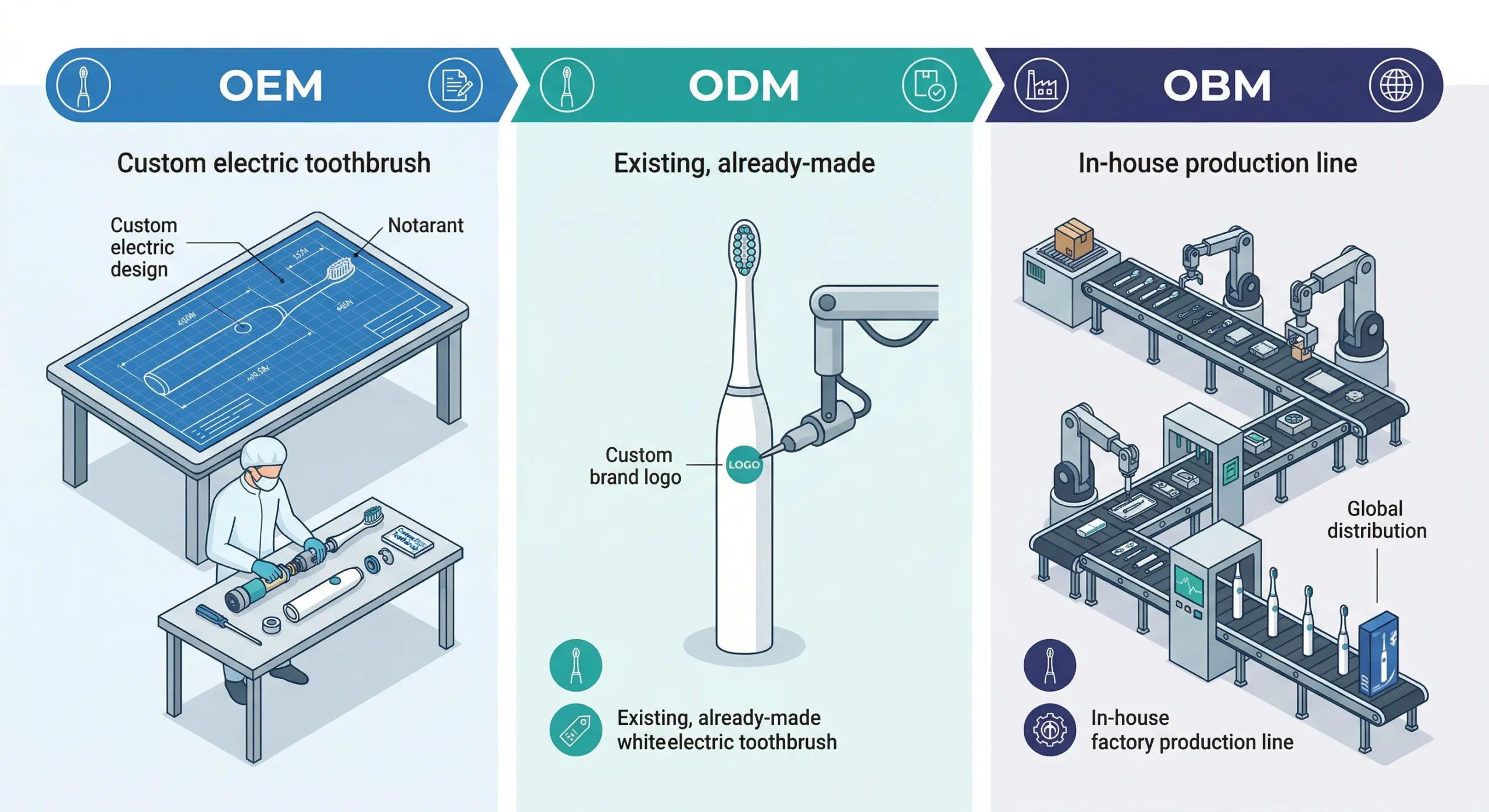

OEM Manufacturing Opportunity Analysis

China as the Dominant Manufacturing Hub

China's electric toothbrush manufacturing ecosystem is unmatched in scale, capability, and cost efficiency. For a detailed walkthrough of the OEM process, see our electric toothbrush OEM manufacturing guide. The Shenzhen-Dongguan corridor in Guangdong Province is home to the majority of OEM/ODM production, with an estimated 300+ factories producing electric oral care devices for the global electric toothbrush market. This concentration creates deep supply chain advantages: raw material suppliers, mold makers, motor manufacturers, battery producers, PCB assembly facilities, and packaging printers are all within a 60-minute radius, enabling compressed lead times and rapid iteration.

Beyond cost, China's manufacturing advantage increasingly lies in engineering capability. Leading OEM factories employ 50–200+ engineers and offer full-service product development, from industrial design and mechanical engineering to firmware development and app integration. The quality gap between Chinese OEM output and Western-branded products has narrowed dramatically, with many Chinese-manufactured devices meeting or exceeding the build quality of branded alternatives.

Shenzhen vs. Competing Manufacturing Regions

While Vietnam, India, and Mexico are frequently discussed as alternative manufacturing destinations, China retains decisive advantages for electric toothbrush market production. The key comparison points include:

- Supply chain depth: Shenzhen offers complete vertical integration — motor suppliers, battery manufacturers, injection molders, PCB fabricators, and assembly lines are all co-located. Vietnam and India lack equivalent supply chain density for precision motor assemblies.

- Engineering talent: China produces approximately 6 million STEM graduates annually. Shenzhen OEM factories routinely offer firmware development, PCB layout, and industrial design services that competing regions cannot match at comparable costs.

- Lead times: Standard production lead times in Shenzhen are 25–35 days from order confirmation to shipment. Comparable facilities in Vietnam typically require 40–55 days due to component import dependencies.

- Cost competitiveness: Despite rising labor costs, total unit costs in Shenzhen remain 20–35% lower than Vietnam and 40–50% lower than Mexico for equivalent electric toothbrush specifications.

MOQ and Cost Trends

Minimum order quantities and unit costs in the electric toothbrush market vary significantly by product complexity and customization level:

- Standard sonic toothbrush (off-tooling): MOQ 500–1,000 units, unit cost $4–$8

- Custom sonic toothbrush (new mold): MOQ 1,000–2,000 units, unit cost $8–$15, mold fee $3,000–$8,000

- Smart connected toothbrush: MOQ 1,000–3,000 units, unit cost $15–$25

- Premium smart toothbrush (AI + app): MOQ 2,000–5,000 units, unit cost $25–$35

For a deeper cost analysis, see our руководство по стоимости производства электрических зубных щеток. Cost trends in 2026 are characterized by modest deflation on standard components (motors, batteries, plastics) and modest inflation on advanced components (BLE modules, MEMS sensors) due to ongoing semiconductor supply normalization. Overall, unit costs in the electric toothbrush market have remained stable or declined 2–5% year-over-year for equivalent specifications.

OEM Sourcing Essentials

- MOQ: 500–2,000 units for standard models; 2,000–5,000 units for premium smart toothbrushes

- Время выполнения: 25–35 days standard production; 40–55 days for custom tooling and initial production runs

- Контроль качества: AQL 1.5 for major defects, AQL 2.5 for minor defects — compliant with ISO 2859-1 sampling standards

- Factory Scale: 20,000m² facility with 300+ employees, 15 production lines, and 50+ in-house R&D engineers at Relish Technology

- Сертификаты: FDA, CE (MDR), ISO 13485, RoHS, REACH, UN 38.3 pre-certified — reducing market entry lead time by 3–6 months

Certification Landscape

Electric toothbrush market access requirements vary significantly by destination. OEM manufacturers targeting the European market must comply with CE marking under the Medical Device Regulation (MDR) or the Electromagnetic Compatibility Directive, depending on product classification. The US market requires FDA registration or 510(k) clearance for most electric toothbrushes. Additional certifications commonly required include RoHS, REACH, UN 38.3 (battery safety), and IPX7 (waterproof rating). For manufacturers like Relish Tech, maintaining pre-existing certification portfolios dramatically reduces time-to-market for new brand partners. See our руководстве по OEM-сертификации for a complete breakdown of requirements by market.

Ready to Launch Your Electric Toothbrush Line?

Talk to our engineering team about your product requirements. We offer integrated hardware-plus-software solutions, pre-existing FDA/CE certifications, and 25–35 day standard lead times.

Talk to Our Engineering TeamStrategic Recommendations for Market Entrants

Based on our analysis of the current market landscape, we offer the following strategic recommendations for companies considering electric toothbrush market entry:

- Target a specific niche first. Rather than competing head-to-head with Philips and Oral-B, identify an underserved segment — such as orthodontic patients, seniors, children, or eco-conscious consumers — and build your brand identity around that niche before expanding.

- Lead with one hero product, not a full range. Successful new brands typically launch with a single well-differentiated SKU rather than a product lineup. Concentrate your development budget, marketing spend, and brand narrative on making one exceptional product.

- Invest in the companion experience. For smart toothbrushes, the app is not an afterthought — it is the product. Allocate 20–30% of your development budget to software, and prioritize user experience over feature count.

- Build the subscription model from day one. The economics of the electric toothbrush market only work at scale when recurring revenue from replacement heads is factored in. Design your packaging, onboarding, and follow-up communications to maximize subscription conversion.

- Choose your manufacturing partner based on R&D capability, not just unit cost. The best OEM partners provide product engineering input, regulatory guidance, and ongoing quality improvement — capabilities that justify a modest per-unit premium and dramatically reduce your total cost of ownership.

- Plan for regulatory diversity from the start. If you intend to sell across multiple markets, design your product to meet the most stringent regulatory requirements (typically EU CE + US FDA) from the outset. Retrofitting compliance adds cost and delays.

8 Key Takeaways

- The $4.36B electric toothbrush market will reach $6.82B by 2030 (7.8% CAGR)

- Asia-Pacific is the fastest-growing electric toothbrush market region at 9.8% CAGR

- Smart/app-connected toothbrushes grow at 14.2% CAGR — double the overall electric toothbrush market rate

- Sonic technology holds 55% market share and commands a price premium

- OEM costs range $4–$35/unit; retail prices range $25–$350+

- China's Shenzhen hub offers 25–35% cost advantage over competing regions

- Sustainability features command 15–25% premium in European markets

- Subscription models deliver 3.2x higher customer lifetime value

Enter the Electric Toothbrush Market with Confidence

Relish Technology provides end-to-end OEM manufacturing for electric toothbrushes — from product design and prototyping through production, certification, and global logistics. With 20,000m² of manufacturing space, 300+ employees, and pre-existing FDA/CE/ISO 13485 certifications, we reduce your time-to-market by 3–6 months.

Request a Manufacturing QuoteЧасто задаваемые вопросы

Ссылки

- Grand View Research. (2025). Electric Toothbrush Market Size, Share & Trends Analysis Report, 2025–2030. Извлечено из https://www.grandviewresearch.com/industry-analysis/electric-toothbrush-market

- Statista. (2026). Electric Toothbrushes: Worldwide Market Data & Revenue Forecasts. Извлечено из https://www.statista.com/outlook/cmo/beauty-personal-care/oral-care/electric-toothbrushes/worldwide

- Mordor Intelligence. (2025).

. Electric Toothbrush Market — Growth, Trends, and Forecasts (2025–2030). Извлечено из https://www.mordorintelligence.com/industry-reports/electric-toothbrush-market - World Health Organization. (2022). Global Oral Health Status Report: Towards Universal Health Coverage for Oral Health by 2030. Geneva: WHO. Retrieved from https://www.who.int/publications/i/item/9789240061484

- Euromonitor International. (2025). Oral Care: Global Industry Overview and Market Data. Passport database. Retrieved from https://www.euromonitor.com/oral-care

- United Nations, Department of Economic and Social Affairs. (2023). World Population Ageing 2023. Извлечено из https://www.un.org/development/desa/pd/

- Американская стоматологическая ассоциация. (2024). Consumer Oral Health Behavior Survey. Извлечено из https://www.ada.org/resources/research